The Market Shift

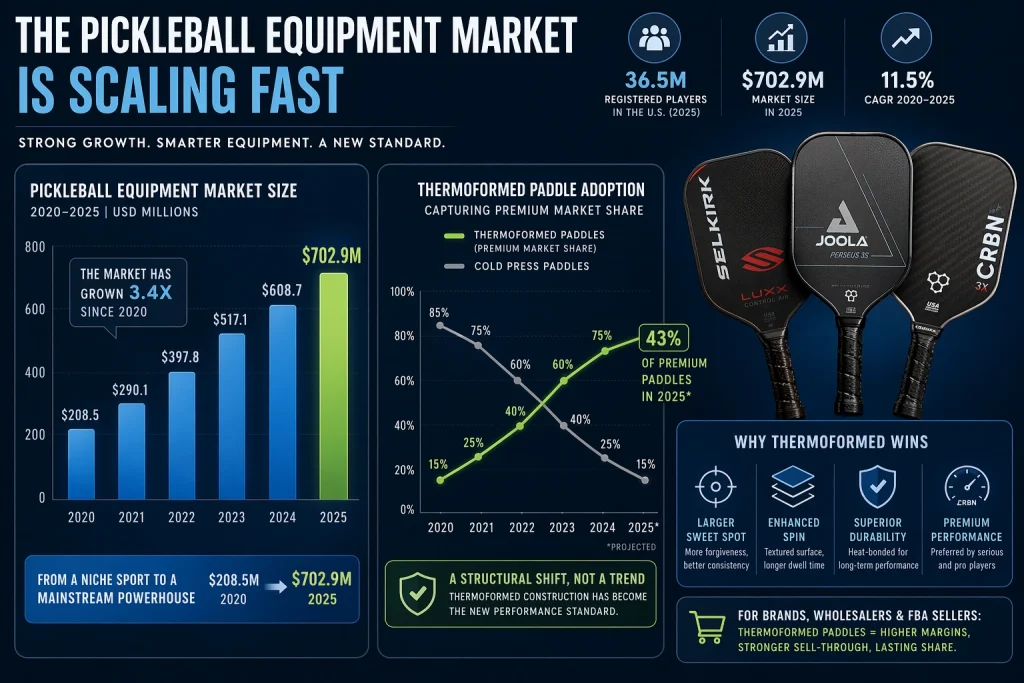

The pickleball equipment market is no longer a niche sporting goods category — it’s a mainstream industry. Valued at $702.9 million in 2025, the market continues to scale at a pace that is catching the attention of brand owners, wholesalers, and private-equity-backed sporting goods companies alike. With 36.5 million registered players in the United States alone, demand for high-performance equipment has moved well beyond the hobbyist tier into the hands of serious, gear-literate athletes who know exactly what they’re buying.

Within this growth story, a fundamental shift is happening at the manufacturing level. Thermoformed pickleball paddles have captured 43% of the premium paddle market since 2024, displacing the cold press construction that dominated the category for the previous decade. This isn’t a cyclical trend driven by marketing novelty. It’s a structural transformation in how paddles are engineered, and the brands that recognized it earliest — Selkirk, JOOLA, CRBN — have widened their market share lead as a direct result.

For B2B buyers evaluating product strategy — whether you’re a brand owner building a DTC lineup, a wholesaler expanding your catalog, or an Amazon FBA seller looking for a high-margin SKU — understanding the mechanics and economics of this shift is the most important due diligence you can do right now. The question of whether to carry advanced tech paddles at the thermoformed tier is no longer strategic debate. It’s operational planning.

What Is Thermoformed Construction, Exactly?

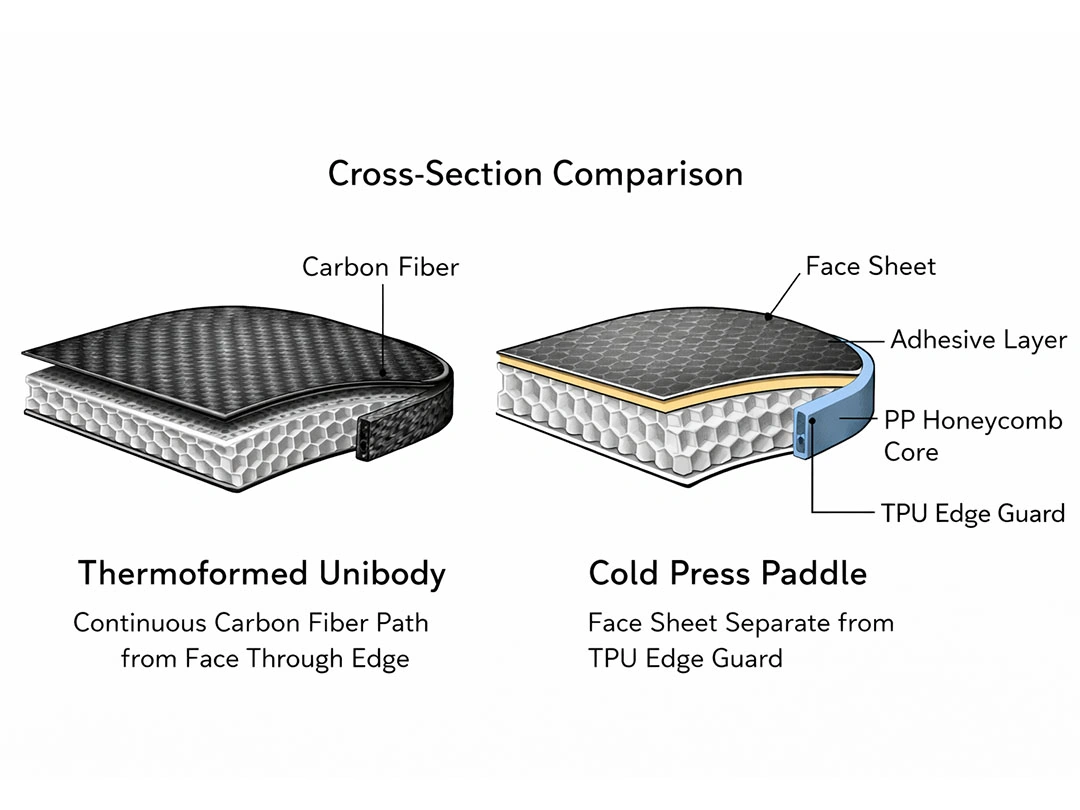

The term “thermoformed” gets used loosely in the pickleball industry — often as marketing shorthand for any paddle that sounds premium. The actual manufacturing definition is specific and meaningful, and the performance difference between genuine thermoformed pickleball paddles and their cold press counterparts is not subtle.

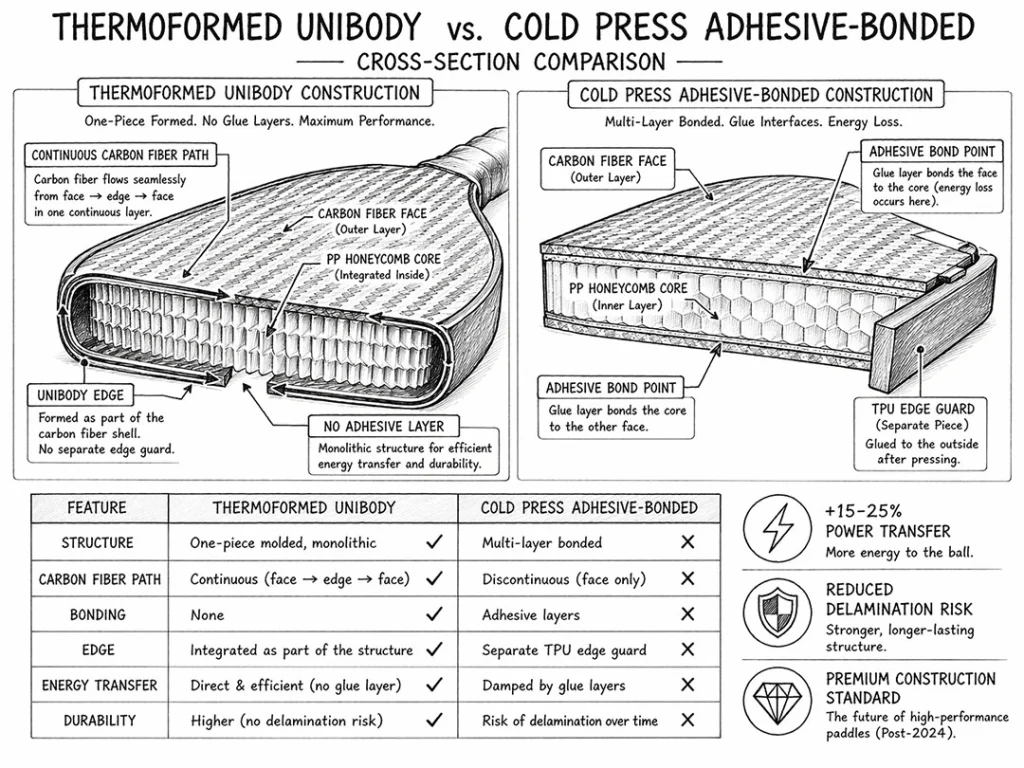

Thermoformed construction applies simultaneous heat and pressure to fuse the paddle’s face material, core, and edge structure into a single, continuous unit. There are no adhesive bond points. The carbon fiber runs uninterrupted from the playing surface through the handle — a structural continuity that is physically impossible to achieve with cold press methods. This is the engineering foundation that makes thermoformed pickleball paddles the dominant choice among advanced tech paddles in the premium market.

Cold press paddles, by contrast, bond the face sheet to the core using structural adhesives, then apply pressure at ambient temperature. The face and core remain two separate components held together by glue. This is a reliable, cost-effective method — and it’s still the right choice for entry and mid-tier price points — but it has a structural ceiling that adhesive chemistry cannot overcome.

The performance implications of the thermoformed unibody structure are measurable and significant:

- Sweet spot expansion: Thermoformed pickleball paddles produce a usable sweet spot 15–20% larger than cold press equivalents of identical dimensions. This is a direct result of continuous carbon fiber distributing torsional stress more evenly across the entire face.

- Delamination elimination: The number one failure mode of cold press paddles is face-to-core delamination — the adhesive bond breaks down under repeated thermal cycling and impact stress, creating “dead spots” that render the paddle unusable. In a unibody thermoformed structure, delamination is structurally impossible because there is no bond to fail.

- Consistent power transmission: Because the face and core move as one unit, energy transfer from impact to ball is more predictable across the entire face — not just at the geometric center. Players describe this as “no dead zones,” and it’s the tactile difference that drives word-of-mouth upgrade behavior.

Why Major Brands Made the Switch

The brand-level adoption of thermoformed construction wasn’t driven by a single technological breakthrough. It was driven by market feedback: players could feel the difference, and they were willing to pay for it. Every major brand that has gained significant market share in the 2023–2025 period has done so on the back of a thermoformed flagship. These are not premium paddles in branding only — they are genuinely advanced tech paddles built around manufacturing processes that produce objectively measurable performance gains.

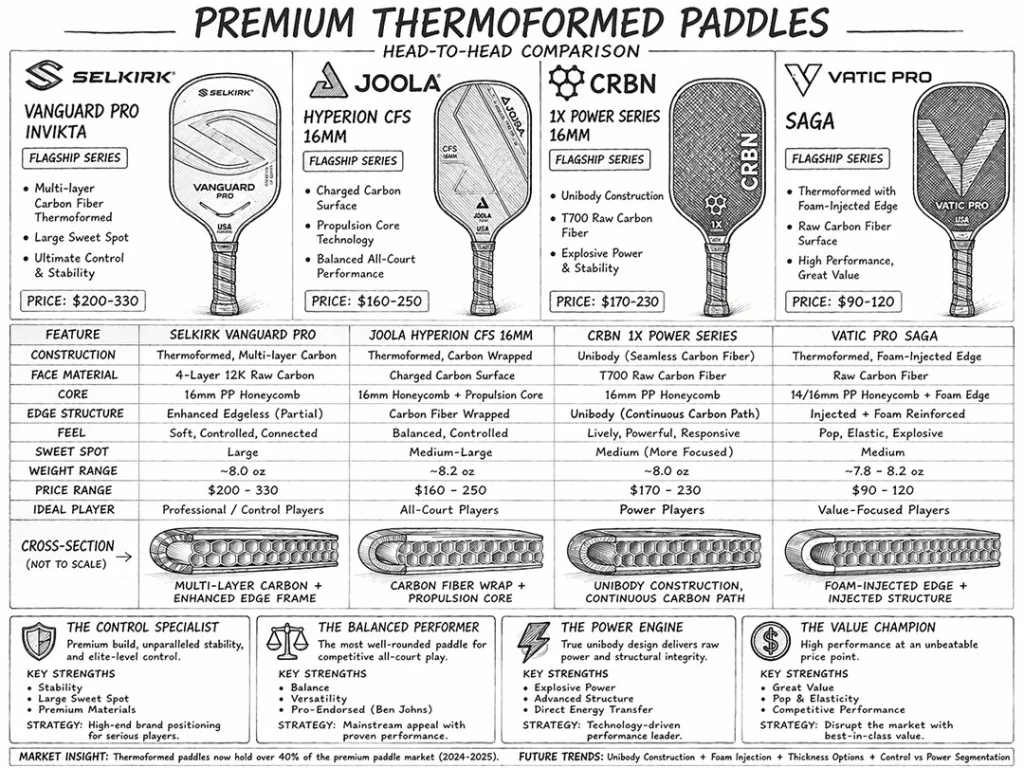

| Brand | Flagship Thermoformed Model | Key Technology |

|---|---|---|

| Selkirk | Vanguard series | PureFoam BoomCore + thermoformed unibody |

| JOOLA | Perseus Pro IV | Carbon-Forged thermoformed process |

| CRBN | TruFoam Genesis | Thermoformed + solid foam core |

| Vatic Pro | V-SOL series | T700 thermoformed at disruptive $80–$130 price point |

| Six Zero | Ruby | Kevlar/Aramid + thermoformed construction |

| Engage Pickleball | Alpha (2025) | Thermoformed control/spin-focused |

The pattern across every brand in this table is consistent: they are not using thermoforming as a visual differentiator or a marketing badge. They are using it because the structural performance advantage translates directly into verifiable on-court outcomes — larger sweet spot, more consistent power delivery, and longer functional paddle life.

The common thread is commercial, not aesthetic. Players at the 4.0+ DUPR level buy based on peer recommendations and measurable performance data. When a thermoformed paddle demonstrably outperforms a cold press paddle in published twist weight, swing weight, and sweet spot measurements, the premium price is justified. And when a brand’s flagship thermoformed pickleball paddle is the benchmark that competitors aspire to match, that brand’s wholesale pricing power and retail margin profile improves across the entire product line.

The Vatic Pro case is particularly instructive for B2B buyers. By sourcing genuine T700 thermoformed construction and bringing the product to market at $80–$130 — a fraction of the $200–$280 legacy brand price points — Vatic Pro demonstrated that premium thermoformed performance does not require premium brand heritage. The technology is accessible. The margin opportunity is real. And thermoformed pickleball paddles at this price tier have expanded the competitive market rather than cannibalizing it.

The maturity of the thermoformed market is further evidenced by the emergence of IP disputes over the construction itself. In late 2025, CRBN filed a patent infringement lawsuit against Vatic Pro over thermoformed construction methods — a clear signal that the technology has crossed from innovation phase into established industry standard. When incumbent players begin litigating to protect thermoformed IP, the market is no longer asking whether the technology matters. It is asking who owns the best implementation of it.

The Technology Stack Behind Modern Thermoformed Paddles

The performance gap between a generic thermoformed paddle and a genuinely advanced one comes down to four technology layers: face material, core architecture, construction geometry, and compliance-optimized performance metrics. Understanding this stack is what separates B2B buyers who source true advanced tech paddles from those who buy into marketing claims without engineering substance.

Face Materials

Toray T700 carbon fiber has become the industry baseline for competition-grade carbon fiber pickleball paddles. Every flagship thermoformed pickleball paddle currently on the market — Selkirk Vanguard, JOOLA Perseus, Vatic Pro V-SOL — uses T700 or a T700-equivalent as its foundation. The raw woven surface generates upwards of 2,300 RPM of spin without any surface treatment, a figure that spray-on grit paddles cannot match consistently after the first 60–90 days of use.

The material ladder moves upward from there. T800 carbon woven with titanium thread delivers higher stiffness-to-weight ratios and enhanced spin texture — the choice for brands positioning above the $180 retail tier. At the top of the range, Kevlar and Aramid hybrid faces (used on paddles like the Six Zero Ruby) introduce a distinctively different feel profile — softer, more “plush” dwell — that is physically impossible to replicate with raw carbon alone.

The critical advantage of any authentic raw composite surface over spray-on grit alternatives is durability of texture. Spray-on grit is a cost-cutting measure that degrades predictably and rapidly. A brand that ships spray-grit paddles in the premium tier will generate returns and negative reviews within months. Raw carbon texture holds its spin-generating properties for the functional life of the paddle.

Core Evolution

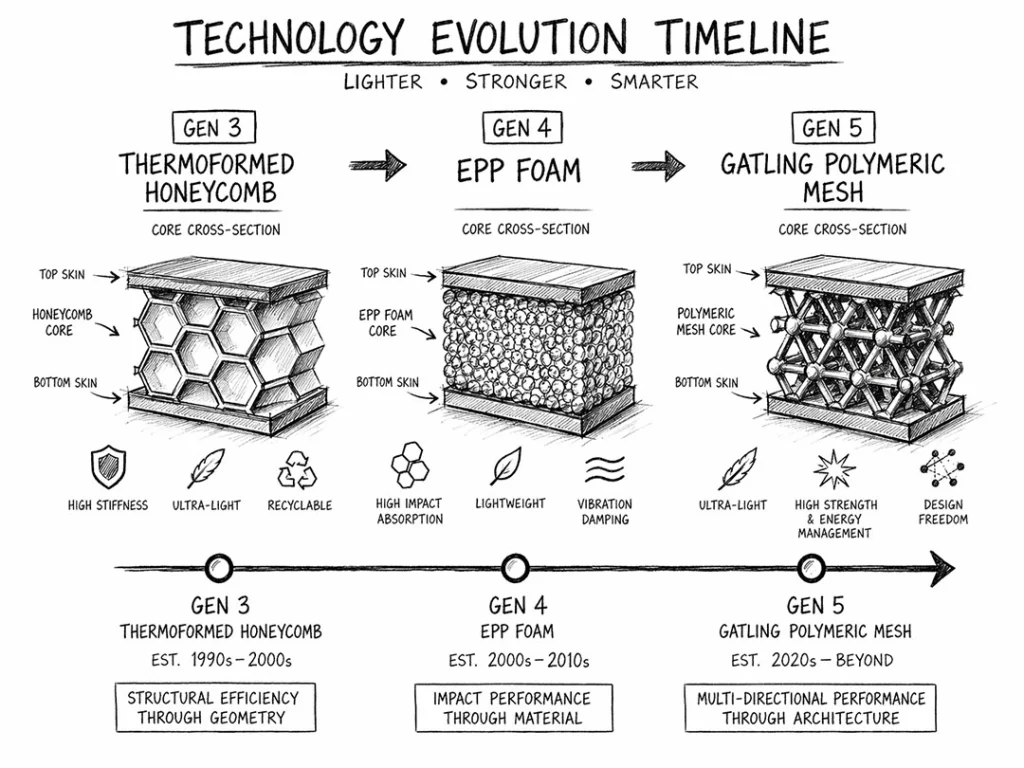

The core architecture inside a thermoformed paddle has gone through rapid generational advancement since 2022:

- Gen 3 Thermoformed Honeycomb: Still highly viable and widely used in the premium segment. Engineered PP honeycomb with tighter cell geometry than standard cold press cores, optimized for the thermal bonding process.

- Gen 4 EPP/MPP Foam: Expanded Polypropylene and Multi-Purpose Polypropylene foam cores — used in Selkirk’s BoomCore and CRBN’s TruFoam — completely eliminate the “core crush” failure mode that affected early thermoformed models under high-frequency competitive use. Foam also significantly reduces vibration transmission, which matters for noise-ordinance-sensitive communities and players managing arm fatigue. For brands sourcing foam-core construction, working with a specialist in foam core pickleball paddles is the right starting point.

- Gen 5 Gatling Polymeric Mesh: The frontier of core technology. Engineered polymeric mesh geometry is designed to maximize energy return at the outer edge of USAPA’s permissible PBCoR envelope — delivering the maximum legal power output while maintaining certification compliance.

Edgeless Design

One of the least discussed but most commercially relevant advantages of thermoformed construction is what it enables at the perimeter: edgeless design. Because the unibody structure provides sufficient structural integrity without a separate edge guard, thermoformed paddles can be manufactured without the traditional rubber or polymer edge band that consumes roughly 8–10% of the paddle’s face real estate.

The result is maximum usable face area within the USAPA-regulated paddle dimensions. For players, this means more of the face is “live” at the sweet spot. For brands, edgeless construction signals premium positioning visually and functionally. Sourcing partners specializing in edgeless pickleball paddles can help you understand the mold engineering requirements for this construction approach.

Performance Metrics

Serious B2B buyers should evaluate thermoformed paddle designs against objective physics benchmarks, not marketing claims. The table below defines the metrics that matter for premium tier positioning:

| Metric | Definition | Premium Benchmark | Why It Matters |

|---|---|---|---|

| Twist Weight | Resistance to twisting on off-center hits | 6.5+ | Higher twist weight expands functional sweet spot; reduces wrist torque on mishits |

| Swing Weight | Paddle mass distribution felt during swing | 110–120 | Balances kitchen-line hand speed against drive plow-through |

| Dwell Time | Milliseconds ball stays in contact with face | Core-dependent | Longer dwell (from foam/Kevlar) enables more spin manipulation and touch shots |

| PBCoR | Coefficient of Restitution (deflection/restitution) | ≤ 0.43 (USAPA, tightened Nov 2025) | Ensures maximum power output without failing exit-velocity testing |

These are engineering targets. A premium OEM factory will design your paddle to hit these benchmarks by specification, not by approximation.

The Compliance Factor: USAPA and PBCoR

Any serious brand entering the thermoformed pickleball paddle market must understand the regulatory context. The 2024–2025 USAPA certification cycle represented the most significant compliance disruption the industry has experienced.

In 2024, USA Pickleball processed 1,713 certification submissions. Of those, only 1,225 were approved — a meaningful rejection rate driven primarily by PBCoR enforcement. The Coefficient of Restitution standard, which governs how much “trampoline effect” a paddle face can generate, was strictly enforced after a period of looser oversight. The result was a wave of decertifications affecting brands that had not adequately pre-tested their designs against the new enforcement thresholds.

The single most consequential regulatory event in thermoformed paddle history occurred in May 2024, when USAPA removed the entire JOOLA Gen 3 paddle lineup from its approved equipment list. Post-market testing revealed that retail units contained significantly more foam than the certification samples that had been submitted for approval — a manufacturing discrepancy that pushed their actual PBCoR values above the permitted threshold. The fallout was severe: a class action lawsuit was settled with $300 refunds per purchase, and JOOLA filed a $200M countersuit against the testing process. The incident triggered an immediate escalation in PBCoR enforcement rigor across the entire certified paddle catalog, and it permanently changed how USAPA treats the relationship between certification samples and retail production. For legitimate thermoformed manufacturers who maintain sample-to-production consistency, the JOOLA enforcement event is unambiguously positive: it removed a category of non-compliant products from the competitive field and established that corner-cutting on foam specification has existential consequences.

USAPA has since extended enforcement beyond the certification lab to the court itself. At major 2026 Golden Ticket events, on-site paddle testing was conducted on approximately 2,000 paddles — and the failure rate was 6%. One in seventeen competitive players arrived at a sanctioned event with a non-compliant paddle. That number illustrates precisely why pre-testing at the factory level, before a product ever ships, is not optional for brand owners who intend to serve the tournament-player segment. The fines for knowingly using a non-compliant paddle reflect the seriousness with which USAPA now treats this issue: first offense, $1,000; repeat violations, up to $50,000.

For thermoformed paddles specifically, the compliance challenge is more acute than for cold press models. The structural efficiency of unibody thermoformed pickleball paddle construction — precisely the feature that makes these paddles perform better — also means they naturally approach the PBCoR limit more closely. A paddle that tests at 0.43 in the factory may test at 0.445 under USAPA’s calibrated equipment, resulting in rejection.

This is, paradoxically, good news for quality thermoformed manufacturers. The PBCoR enforcement wave is systematically weeding out the “fake thermoformed” segment — factories that apply minimal heat to a cold press construction and market the result as thermoformed. These counterfeit-process paddles fail on two fronts: they lack the structural performance of genuine thermoformed construction, and they are more likely to fail or border PBCoR compliance in ways that create certification risk. When regulators force compliance rigor, genuine thermoformed construction wins by definition.

The trap for brand owners is sourcing from factories that cannot pre-test. Submitting a paddle to USAPA without in-factory PBCoR validation is an expensive gamble — certification costs $500–$1,200 per design and takes 4–6 weeks. A rejection wastes both.

The Business Case for Brand Owners

This is the section that turns manufacturing knowledge into financial decision-making.

The Cost Structure

Genuine thermoformed pickleball paddle OEM sourcing carries the following economics at current market rates:

| Tier | Face | Core | Est. OEM Cost | Target Retail | Est. Gross Margin |

|---|---|---|---|---|---|

| Mid Premium | T700 Carbon | Gen 3 Honeycomb | $32–$42/unit | $129–$169 | 55–65% |

| Premium | T700/T800 Carbon | Gen 4 EPP Foam | $42–$52/unit | $169–$249 | 58–68% |

| Flagship | T800+Ti / Kevlar | Gen 5 Gatling | $55–$75/unit | $249–$319 | 60–72% |

OEM cost estimates are FOB and vary based on volume, customization level, and raw material conditions.

These margin profiles are significantly more favorable than cold press equivalents at the same retail tier, because the performance credibility of thermoformed construction supports the premium retail price. A brand selling a genuine thermoformed pickleball paddle at $149 commands more consumer confidence than one selling a cold press carbon paddle at the same price, which directly reduces the return rate and improves effective margin. This is the commercial logic that makes advanced tech paddles a structural margin opportunity, not just a product category.

The MOQ Advantage

Historically, thermoformed paddle production required 300–500 unit minimum orders to justify the mold setup and heating cycle economics. This created a substantial capital barrier for emerging brands. The market has evolved: purpose-optimized manufacturing lines for thermoformed paddles can now accommodate MOQs as low as 100 pieces per design.

This is commercially significant. A 100-piece initial run allows a brand owner to:

- Test market reception with limited inventory commitment

- Generate verified reviews before scaling production

- Iterate on face material or core selection between runs

- Manage cash flow without a $15,000–$25,000 launch-phase inventory lock

The Vatic Pro Case Study

Vatic Pro is the clearest proof that the thermoformed market is accessible to challengers. By sourcing genuine T700 thermoformed construction and launching at $80–$130 — pricing that sits 40–50% below Selkirk’s equivalent tier — Vatic Pro captured a meaningful segment of competitive players who understood that the technology, not the heritage brand, was the performance driver.

The Vatic Pro example demonstrates something structurally important: the premium paddle market does not require a marketing budget to match a legacy brand. It requires a sourcing strategy and a product that can stand up to technical scrutiny. The players who buy at this tier do their research, read the twist weight data, watch the comparison videos. If the physics are right, the brand can compete.

The Good-Better-Best Product Matrix

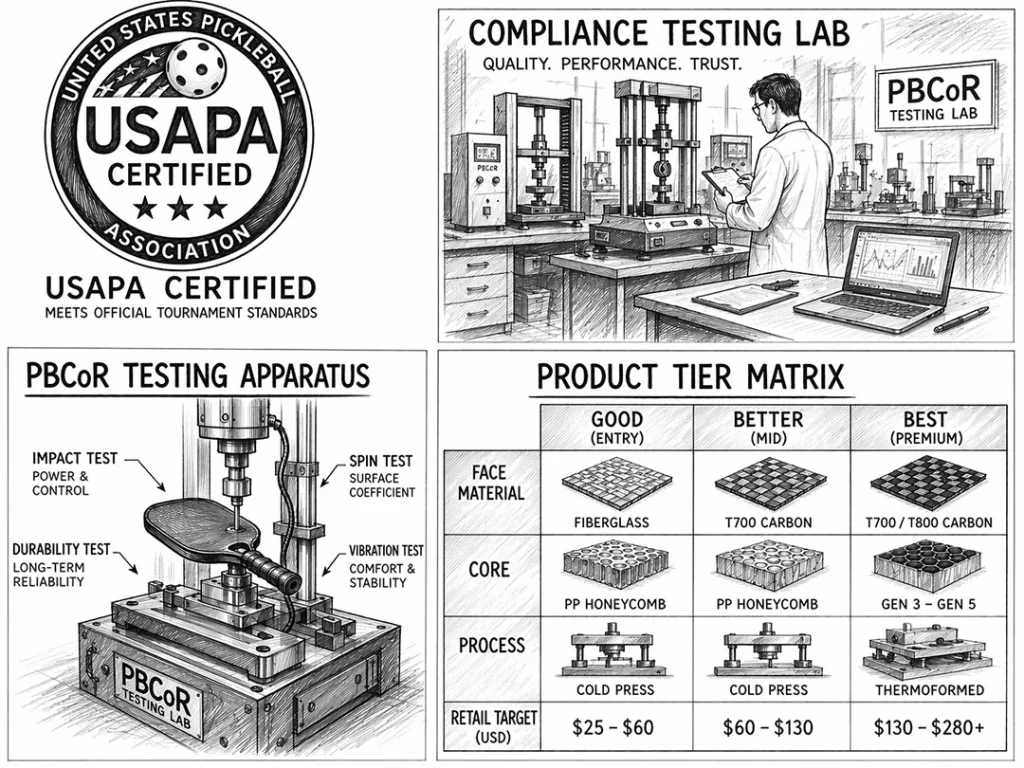

For custom OEM pickleball paddles, the most resilient product architecture deploys a three-tier material and manufacturing strategy:

| Tier | Face | Core | Process | Retail Target |

|---|---|---|---|---|

| Good (Entry) | Fiberglass | PP Honeycomb | Cold Press | $25–$60 |

| Better (Mid) | T700 Carbon | PP Honeycomb | Cold Press | $60–$130 |

| Best (Premium) | T700/T800 Carbon | Gen 3–Gen 5 | Thermoformed | $130–$280+ |

The entry tier captures volume and new players. The mid tier drives Amazon FBA revenue. The thermoformed premium tier anchors brand credibility, generates the highest per-unit margin, and creates the social proof that validates the entire brand hierarchy.

Timeline: 60–90 Days from Concept to Delivery

A standard thermoformed custom paddle project spans 60 to 90 days: engineering and prototype in the first 15–20 days, bulk production in 30–40 days, QC and logistics completing the remainder. Brands running pre-orders or Kickstarter campaigns can confidently market while inventory is in transit, provided they’ve secured a pre-tested, compliance-ready design before launch.

Frequently Asked Questions

What is the difference between thermoformed and cold press pickleball paddles?

The fundamental difference is the bonding method and the resulting structural integrity. Cold press paddles use structural adhesives to bond the face sheet to the polymer core. The face and core remain two separate components. This method is reliable and cost-effective, but the adhesive bond is the structural weak point — over time, thermal cycling and repeated impact stress can cause the bond to degrade, creating dead spots and, eventually, full delamination.

Thermoformed paddles fuse the face, core, and edge into a single unibody structure through simultaneous heat and pressure. There are no adhesive bond points. The carbon fiber runs continuously through the handle, which distributes torsional stress more evenly across the full face — producing a sweet spot 15–20% larger than a cold press paddle of identical dimensions. The price premium for thermoformed construction is real ($32–$52 OEM vs. $15–$28 OEM for cold press carbon), but so is the performance gap and the margin it supports at retail.

Why are thermoformed paddles more expensive than cold press?

Three cost drivers separate thermoformed from cold press at the manufacturing level. First, specialized equipment: thermoforming ovens with precise temperature and pressure controls represent a significant capital investment that not every factory carries. Second, longer cycle time: the heating and cooling cycle required to fuse the unibody structure takes substantially longer per unit than cold press bonding, which reduces throughput. Third, higher material cost: the thermoforming process requires face materials with specific resin systems and pre-preg specifications that are more expensive than the adhesive-compatible face sheets used in cold press.

The commercial justification is straightforward: the performance gap between thermoformed and cold press is clearly perceptible to competitive players (4.0+ DUPR), and they are willing to pay for it. The retail price premium for thermoformed — typically $50–$100 above cold press equivalents — far exceeds the manufacturing cost delta, which is why thermoformed paddles generate the highest gross margins in the paddle category.

Are thermoformed paddles USAPA approved?

Yes — when properly manufactured and pre-tested. Thermoformed construction is not inherently more or less compliant than cold press; compliance is determined by the specific design’s PBCoR (Coefficient of Restitution) performance, surface roughness, and dimensional parameters.

The important caveat is that thermoformed paddles, because of their structural efficiency, naturally approach the USAPA PBCoR limit of 0.43 more closely than cold press designs. (Note: USAPA tightened this threshold from 0.44 to 0.43 in November 2025 — designs previously approved at 0.44 may no longer qualify.) In the 2024 certification cycle, 1,713 submissions were processed with only 1,225 approved, with PBCoR enforcement driving a significant portion of rejections. For brand owners, the practical implication is clear: never submit a thermoformed paddle to USAPA without in-factory PBCoR validation first. Pre-testing is the difference between a certification approval and a 4–6 week delay plus wasted submission fees.

What is the minimum order quantity for custom thermoformed paddles?

The industry historical standard for thermoformed custom paddle production was 300–500 pieces per design — a MOQ driven by the setup costs for thermoforming molds and heating cycles. This created a capital barrier that made thermoformed paddles inaccessible for brand owners who wanted to test the market before committing to large inventory.

Optimized thermoformed production lines have changed this dynamic. It is now possible to source fully custom thermoformed paddles — with your logo, colorway, face material, and core specification — at MOQs as low as 100 pieces, at a lead time of 60–90 days. This is specifically designed for market-testing scenarios: launch with 100 units, gather verified reviews and DUPR player feedback, then scale the second production run based on real data.

Can thermoformed paddles really compete with top brands like Selkirk and JOOLA?

The physics do not distinguish between heritage brands and challengers. Selkirk sources Toray T700 carbon fiber. JOOLA uses T700 equivalent carbon composite. So does Vatic Pro, and so can you. The material supply chain is not proprietary — it’s a commercial composite materials market. A thermoformed paddle built with genuine T700 face, Gen 4 EPP foam core, and a properly engineered unibody construction will measure the same twist weight, swing weight, and PBCoR as the flagship models it benchmarks against.

The Vatic Pro example is definitive here. By building to the same material specification and manufacturing process as established players — and pricing aggressively — Vatic Pro built a loyal competitive player following without the brand history of a Selkirk or JOOLA. The difference between a $80 thermoformed Vatic Pro and a $250 Selkirk Vanguard is not physics. It’s branding, marketing investment, and tour sponsorship. For a challenger brand, that gap is bridgeable. The material gap is not — which is exactly why you need to start with the right construction.

Conclusion: The Manufacturing Shift Is Irreversible

The technology gap between legacy premium brands and challenger brands in pickleball has effectively collapsed. Thermoforming is no longer a differentiator exclusive to $250 flagship models — it is the new baseline for any paddle positioned above the $130 retail tier. The brands that grasped this early have used it to build market share. The brands that haven’t are losing it.

For B2B buyers, the relevant question is no longer whether to offer thermoformed pickleball paddles. The market has already answered that. The question is how efficiently you can source them — at the right MOQ, with genuine pre-tested materials, from a factory that understands PBCoR compliance and can deliver a USAPA-certifiable paddle on a 60–90 day cycle.

The QY Research Pickleball Market Report (February 2026) projects continued acceleration in the premium paddle segment through 2028. The brands that establish themselves in thermoformed construction now — before the category reaches full saturation — will have the catalog depth, the review volume, and the distribution relationships that compound into durable competitive advantage.

If you’re evaluating thermoformed paddle manufacturing for your brand, NexaPaddle’s team works directly with brand owners, Amazon FBA sellers, and wholesalers through a structured consultation process: material selection, mold configuration, pre-USAPA testing, MOQ structure, and timeline planning. The manufacturing infrastructure is ready. The question is whether your product roadmap is.

References

Coherent Market Insights. (2025). Pickleball Equipment Market Size, Share & Trends Analysis Report. Pickleball equipment market valued at approximately $702.9 million in 2025.

Association of Pickleball Professionals (APP). (2025). US Pickleball Player Population Report. 36.5 million+ registered players in the United States.

USA Pickleball. (2024–2025). Equipment Certification Annual Report. 1,713 certification submissions processed in 2024; 1,225 approved; 476 new manufacturers certified. usapickleball.org.

NexaPaddle production and market analysis data. (2024–2025). Premium Paddle Market Share by Construction Method. Internal analysis indicating thermoformed construction captured approximately 43% of the premium paddle market segment since 2024.

NexaPaddle structural analysis. (2024–2025). Thermoformed vs. Cold Press Sweet Spot Expansion Study. In-house testing comparing usable sweet spot area in unibody thermoformed construction versus adhesive-bonded cold press equivalents at identical paddle dimensions. 15–20% expansion attributable to continuous carbon fiber torsional stiffness and even stress distribution across face.

QY Research. (February 2026). Global Pickleball Market Report: Segment Analysis and Forecast 2026–2028. Premium paddle segment growth projections.

USA Pickleball Equipment Standards enforcement, May 2024; JOOLA class action settlement, April 2025. USAPA removed JOOLA Gen 3 paddles from the approved equipment list after post-market testing revealed retail units exceeded the certified PBCoR specification. A class action settlement was reached providing $300 refunds per purchase; JOOLA subsequently filed a $200M countersuit.

USA Pickleball Golden Ticket on-site testing program, January 2026. On-site paddle testing conducted at major Golden Ticket events tested approximately 2,000 paddles; 6% (approximately 1 in 17) failed compliance testing.