The crowd says the gold rush is over. The data says the crowd is wrong — and still losing money on generic paddles.

The Contrarian Thesis

Every six months, a new wave of e-commerce commentary declares pickleball “saturated.” The logic is always the same: too many sellers, too many SKUs, margins compressed, move on.

Here’s what that analysis gets wrong: it conflates market crowding at the bottom with market saturation overall.

The bottom is crowded. White-label paddles at $25–40, zero brand differentiation, a race to the lowest price. That segment is brutal, and it should be avoided entirely.

But pickleball as a category? It is not saturated. It is maturing — which is a fundamentally different thing. Mature markets reward brand equity, product differentiation, and repeat purchase cycles. They punish commodity sellers and reward builders.

The data is unambiguous. The opportunity is real. The question is whether you’re going to compete in the right part of the market.

Section 1: The Trend Reassessment — Pickleball Is No Longer a Fad

Let’s start with the numbers that matter.

24.3 million. That’s the number of active pickleball players in the United States as of 2025, according to the SFIA 2026 Topline Participation Report [1]. That figure represents +22.8% year-over-year growth and a +171.8% increase over three years. For context: tennis has roughly 23 million US players and has been a mainstream sport for decades.

Globally, the pickleball equipment market was valued at $702.9 million in 2026 and is projected to reach $1.85 billion by 2033, growing at a 14.8% CAGR [2]. That’s not a fad trajectory. That’s a category in structural expansion.

But the more important shift isn’t the headline growth number — it’s the player profile change.

In 2021, the average pickleball player was a retiree playing twice a week at a community center. In 2026, the fastest-growing segment is competitive players aged 18–45 who play 4–6 times per week, participate in USAPA-sanctioned tournaments, and treat equipment selection with the same seriousness as a competitive tennis player.

This matters enormously for FBA sellers because of one word: repurchase.

Casual players buy one paddle and use it for years. Competitive players replace paddles every 3–6 months — due to face wear, delamination, or simply chasing the next performance upgrade. A customer who buys your $150 paddle in January is a potential repeat buyer in April. That’s a repurchase engine that doesn’t exist in most Amazon categories.

Amazon sold an estimated $44 million worth of pickleball paddles in 2025 alone [3]. That number is growing. The question isn’t whether the market is there — it’s whether your brand is positioned to capture the high-value segment of it.

Section 2: The Dead-End of the Price War

Here’s the trap that kills most new FBA sellers in this category.

They source a generic paddle from a factory, slap a logo on it, list it at $34.99, and wonder why they’re not profitable. The math is simple and brutal:

- Wholesale cost: $12–18 (generic cold press, no differentiation)

- Amazon fees + FBA: ~$8–10

- PPC advertising: $6–12 per unit sold (competitive keywords)

- Returns: 8–12% return rate on generic paddles (buyers can’t tell the difference, so they return when disappointed)

- Net margin: 15–25% on a good day. Often negative after returns.

This is the white-label commodity trap. You’re not building a brand — you’re renting shelf space on Amazon at a loss.

The premium segment tells a completely different story. Consider the competitive dynamics between JOOLA and Selkirk on Amazon. JOOLA sold roughly half the unit volume of Selkirk in 2025, yet generated comparable revenue [3]. The mechanism is straightforward: Selkirk’s average selling price is significantly higher, driven by brand equity, USAPA certification, and material differentiation. Premium positioning beats unit volume — every time, in every category.

The lesson for 2026 is not subtle: low-end is where brands go to die. The sellers who entered pickleball at $25–40 are now in a margin compression spiral they cannot escape without a complete brand rebuild. The sellers who entered at $120–180 with differentiated product are building customer lists, generating repeat purchases, and compounding brand equity.

You don’t have to fight that war. You can choose not to enter it.

Section 3: The High-Margin Playbook — How to Actually Stand Out

Three pillars separate the brands that win in 2026 from the ones that don’t.

a) Custom Design & Visual Identity

The first thing a buyer sees on Amazon is the paddle face. Before they read a single word of your listing copy, they’ve already made a subconscious quality judgment based on the visual.

Generic paddles look generic. They have flat, printed graphics that look like they were designed in PowerPoint. They communicate “cheap” before the buyer even checks the price.

Premium paddles look premium. The difference is the manufacturing process.

UV printing on flat-surface cold press paddles delivers full-color, photorealistic graphics — gradients, complex illustrations, brand colors rendered with precision. Hydrographic transfer (water decal) on thermoformed paddles wraps seamlessly around the paddle’s three-dimensional curved surface, producing a finish that looks painted-on rather than printed. No seams. No edge buildup. The kind of finish that makes a buyer pick up the paddle in a store and say “this feels expensive.”

That visual quality is the difference between a $40 price point and a $140 price point. The manufacturing cost difference is far smaller than the retail price difference. That gap is your margin.

Brands investing in custom OEM pickleball paddles with proper graphics technology are consistently commanding $120–180 retail versus $40 for visually generic alternatives. The visual identity alone justifies the premium — before the buyer even considers the materials.

b) Frontier Materials — The Technical Moat

This is where the real differentiation lives, and where most sellers don’t go deep enough.

The material stack of your paddle determines its performance characteristics, its price ceiling, and its defensibility against copycat competition. Here’s what the premium tier looks like in 2026:

T800 Toray Carbon Fiber is the flagship face material for serious performance paddles. Compared to the more common T700 carbon fiber, T800 offers higher tensile strength, greater stiffness-to-weight ratio, and superior energy transfer on contact. It’s the material used by the brands that charge $180+ and justify it. If your paddle spec sheet says T700, you’re mid-tier. T800 puts you in the conversation with the category leaders.

Kevlar (Aramid) face material is the choice for players who want vibration dampening combined with power. Kevlar’s fiber structure absorbs shock differently than carbon fiber, producing a softer feel at contact while maintaining pop. JOOLA’s Perseus line uses Kevlar-composite construction — it’s not a niche material anymore, it’s a premium-tier standard.

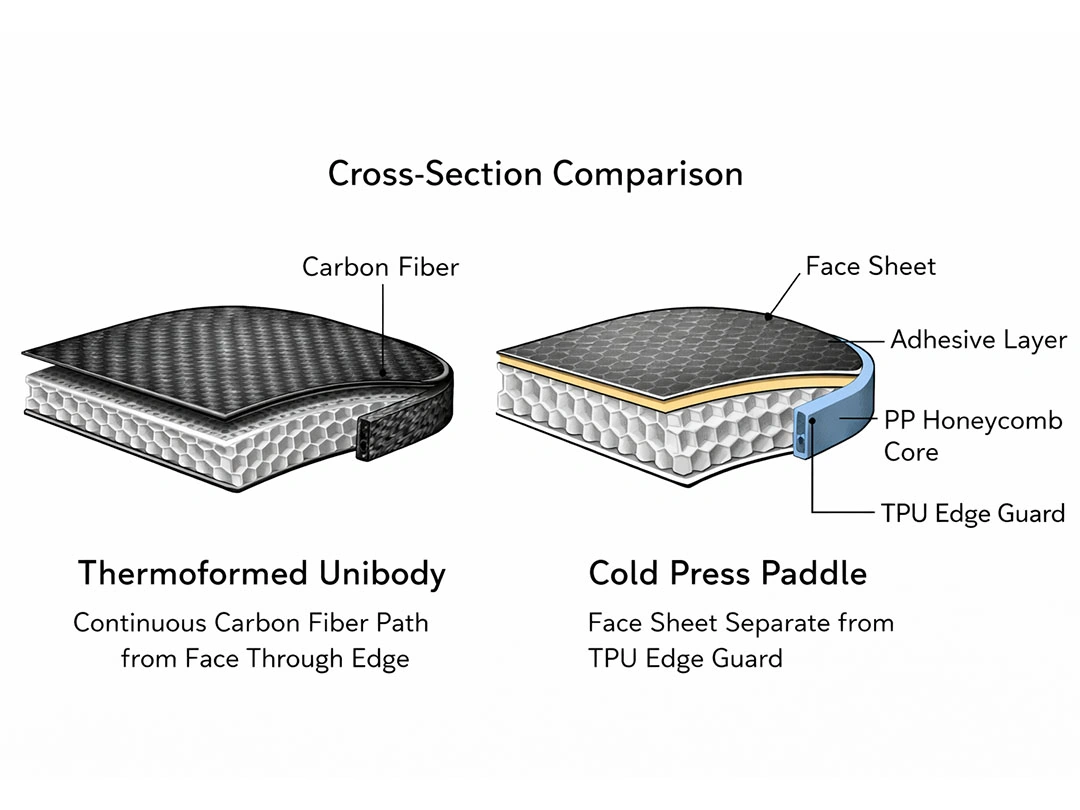

Gen 3 / Gen 4 thermoformed construction with EPP foam cores represents the current state of the art in paddle engineering. Thermoforming — the process of heat-forming the paddle face under pressure — produces a denser, more consistent bond between face and core than cold press manufacturing. The result is better power transfer, more consistent deflection, and a paddle that performs more predictably across its entire face. Thermoformed pickleball paddles at this construction level wholesale at $32–45 and retail at $120–180 with 50%+ gross margins.

Titanium thread reinforcement in the face material adds structural stability that prevents the micro-delamination that degrades paddle performance over time. For competitive players who replace paddles every 3–6 months, a paddle that maintains its performance characteristics longer is a meaningful differentiator — and a reason to stay loyal to your brand.

The combination of T800 carbon fiber face, thermoformed construction, EPP foam core, and titanium reinforcement is not exotic manufacturing — it’s available from the right OEM partners. But it requires knowing what to specify, and it requires a manufacturer with the equipment and QA infrastructure to execute it consistently.

That material stack is your technical moat. A competitor can copy your logo. They cannot easily copy your material specification, your construction process, and your quality consistency simultaneously.

c) USAPA Certification — The Credibility Multiplier

USAPA (USA Pickleball Association) certification is the single most underutilized conversion lever in the Amazon pickleball category.

Here’s what certification does for your business:

Tournament eligibility: USAPA-approved paddles are the only paddles legal for sanctioned tournament play. The 24.3 million US players include a rapidly growing competitive segment that will not buy a non-certified paddle for serious play. Certification is not optional for this buyer — it’s a filter.

Amazon listing conversion: Buyers who know what USAPA certification means — and competitive players do — use it as a quality signal. A certified paddle listing converts at a meaningfully higher rate than an uncertified one at the same price point, because certification answers the buyer’s implicit question: “Is this paddle actually good, or is it just marketed as good?”

Club and league bulk orders: Clubs, recreational leagues, and corporate event organizers buying paddles in bulk almost universally require USAPA certification. This is a B2B revenue channel that is completely inaccessible to uncertified brands.

The cost: USAPA certification runs approximately $2,000–3,000 per paddle model, with a testing and approval timeline of 6–10 weeks [4]. For a brand launching at $150 retail with 50%+ margins, that cost is recovered in the first 30–40 units sold. The marketing ROI is not close — certification pays for itself quickly and compounds over the product’s lifetime.

The brands that skip certification to save $2,500 are leaving a conversion multiplier on the table and locking themselves out of the B2B channel. Don’t be that brand.

Section 4: From Concept to Cargo — The Manufacturing Reality

The playbook above is only executable if you have the right manufacturing partner. This is where most first-time brand builders hit the wall.

The traditional barrier: Most paddle factories in China require minimum order quantities of 500–1,000 units. For a first-time brand testing a new market, that’s $16,000–45,000 in inventory before you’ve validated a single listing. The capital risk is prohibitive, and the consequence of a failed launch is catastrophic.

The manufacturing landscape has evolved. Manufacturers like NexaPaddle have built infrastructure specifically for brand builders entering the category — with MOQs of 100 units for thermoformed paddles and 300 units for cold press, in-house QA labs equipped with Starrett SR-100 testing equipment for USAPA pre-testing, UV printing and hydrographic transfer capabilities in-house, and full Amazon FBA prep (FNSKU labels, poly bags, suffocation warnings) built into the production workflow.

With 10 years of manufacturing experience and 300+ brands served globally, the operational infrastructure exists to take a brand from design brief to FBA-ready inventory in 30–60 days on a first order — without requiring the capital commitment that used to make this category inaccessible to new entrants.

The barrier to entry for a differentiated, certified, materially premium pickleball paddle brand is lower in 2026 than it has ever been. The barrier to entry for a generic, uncertified, commodity paddle brand is higher than it has ever been, because the market has already filled that space with sellers who are losing money.

The choice of which market to enter is yours.

Bottom Line

Pickleball isn’t the next gold rush. It’s the gold rush that’s still happening — just in a different part of the mine.

The $25–40 generic paddle segment is exhausted. Margins are gone, ad costs are punishing, and brand equity is zero. The sellers in that segment are not building businesses — they’re running a slow-motion liquidation.

The $120–180 premium segment — T800 carbon fiber, thermoformed construction, USAPA-certified, visually differentiated — is where the margin lives, where the repeat purchase cycle compounds, and where brand equity actually accumulates.

24.3 million players. $702.9 million market. 14.8% CAGR. 50%+ gross margins for brands that do it right.

The losers in 2026 will be the sellers who chased generic paddles and a race to the bottom. The winners will be the ones who built branded, certified, materially differentiated products that competitive players actually want to buy — and buy again.

The data is not ambiguous. The playbook is not complicated. The only question is whether you execute it.

Frequently Asked Questions

Is pickleball really still growing in 2026, or has it peaked?

The SFIA 2026 Topline Participation Report puts US active players at 24.3 million — up 22.8% year-over-year and 171.8% over three years [1]. Global market projections show a 14.8% CAGR through 2033 [2]. The growth is not in the casual recreational segment, which has plateaued in some markets. It’s in the competitive and semi-competitive player segment, which is expanding rapidly and drives the high-value repurchase cycle. Pickleball has not peaked — it has matured, which is a better condition for brand builders than a fad peak would be.

What’s the realistic gross margin on a private label pickleball paddle?

For a thermoformed paddle with T800 carbon fiber face, sourced at $32–45 wholesale and retailed at $120–180, gross margin runs 50–65% before Amazon fees and advertising. After fees and a reasonable PPC budget, net margin for a well-positioned brand runs 30–45% — compared to 15–25% (often negative after returns) for generic commodity paddles. The margin difference between premium and generic is not incremental. It’s structural.

Do I really need USAPA certification to sell on Amazon?

You can sell without it. You will convert worse, be excluded from the competitive player segment, and be locked out of club and league bulk orders. USAPA certification costs $2,000–3,000 per model and takes 6–10 weeks [4]. For a brand selling at $150 with 50%+ gross margins, that cost is recovered in the first 30–40 units. The ROI is not a close call. Brands serious about building a defensible position in this category get certified.

What’s the minimum order quantity to launch a pickleball paddle brand?

The traditional factory minimum of 500–1,000 units has been the historical barrier. Manufacturers built for brand builders now offer significantly lower thresholds — 100 units for thermoformed paddles, 300 units for cold press, at manufacturers like NexaPaddle. That’s enough inventory to run a genuine market test, validate your listing, and gather real conversion data before committing to a full inventory build. First-order lead times run 30–60 days from design brief to FBA-ready inventory

Sources

- Sports & Fitness Industry Association (SFIA) — 2026 Topline Participation Report. https://www.sfia.org/reports/

- Coherent Market Insights — Global Pickleball Equipment Market Report, 2026–2033. https://www.coherentmarketinsights.com/market-insight/pickleball-equipment-market-4186

- Marketplace Pulse / Jungle Scout — Amazon Pickleball Paddle Category Sales Data, 2025. https://www.marketplacepulse.com / https://www.junglescout.com

- USA Pickleball (USAPA) — Equipment Standards & Approved Paddle List. https://www.usapickleball.org/what-is-pickleball/equipment-standards/

- NexaPaddle — Custom OEM Pickleball Paddles & Thermoformed Paddle Manufacturing. https://nexapaddle.com/custom-oem-pickleball-paddles/