Search “graphite pickleball paddles” today and you’ll find a lot of content that hasn’t caught up with the market. The term still pulls significant search volume — but the buyers typing it are increasingly asking a different question than they were five years ago. They’re not just looking for a graphite paddle to buy. They want to know whether graphite still matters — as a product category, as a sourcing decision, as a business bet.

That’s the right question to ask in 2026. Graphite was the premium material of choice from roughly 2015 through 2020. Today, it occupies a different position in the product hierarchy — one that’s commercially viable but strategically distinct from where the growth is happening. If you’re building or scaling a pickleball paddle line, understanding exactly where graphite sits — and where carbon fiber has taken over — is the difference between a well-structured product ladder and a portfolio that’s chasing a market that moved on.

This article cuts through the terminology confusion, maps the material evolution with market data, and gives B2B buyers a clear framework for how to think about both graphite 그리고 composite pickleball paddles in the context of a 2026 product strategy.

What Are Graphite Pickleball Paddles, Really?

The word “graphite” gets applied loosely in the paddle industry, and that looseness has created genuine confusion for buyers at every level of the supply chain.

At the material science level, graphite in paddle construction refers to a thin crystalline carbon layer — typically a graphite coating or film — applied over a paddle face that is predominantly fiberglass. Graphite is a layered crystalline form of carbon with useful surface hardness and a naturally lubricous feel, but it lacks the tensile architecture of woven carbon fiber. In paddle applications, it primarily contributes surface stiffness to what is otherwise a fiberglass construction.

This is not the same as woven carbon fiber sheets, where continuous carbon filaments are bound with resin to form a structural face material. The distinction matters enormously for performance and for how you position a SKU.

A Brief History: Graphite’s Rise and Repositioning

From 2015 to roughly 2020, graphite-face paddles were the upgrade path. A recreational player starting with a basic aluminum or wood paddle would graduate to a “graphite paddle” as their first real investment in the sport — and that positioning was legitimate at the time. Carbon fiber paddles existed but were priced for professionals and serious amateurs, typically $180–$220+.

The retail channel reinforced this by marketing “graphite” as shorthand for premium, even when the construction was primarily fiberglass with a nominal graphite treatment. Some brands — particularly in the mass-market and entry-level segments — used the term broadly to cover anything that wasn’t straight fiberglass, a practice that persists today.

The result: if you search “graphite pickleball paddle” in 2026, you’ll find products ranging from $30 no-name paddles to mid-range paddles from established brands — but you won’t find elite-tier performance paddles. That tier has moved to carbon fiber.

Graphite vs. Composite vs. Carbon Fiber: Clearing the Terminology Confusion

These three terms appear constantly in product listings, buyer conversations, and sourcing briefs — and they’re not interchangeable. Here’s the hierarchy as it actually exists in 2026:

Material Terminology Table

| Term | 면 소재 | 코어 | 시대 / 시장 위치 | 가격 범위 (소매) |

|---|---|---|---|---|

| 복합재 | 유리섬유 면 + 폴리머 코어 | PP 벌집 구조 | 구형 중급 용어 (2010년대) | $40–$100 |

| 그래파이트 | 유리섬유 기판 위에 얇은 탄소 코팅 | PP 허니콤 또는 노멕스 | 입문에서 중급, 레크리에이션 | $50–$130 |

| 탄소 섬유 (콜드 프레스) | 엮인 UD 또는 3K 탄소 섬유 시트, 차가운 압착 결합 | PP 벌집 구조 | 현재 중급 수준, 강한 가치 | $60–$150 |

| 탄소 섬유 (열형성 T700) | T700 등급 엮인 탄소, 핫프레스 성형 | PP 허니콤 또는 고급 코어 | 현재 프리미엄-성능 | $100–$180 |

| 탄소 섬유 (T800 / 포지드) | T800 탄소 + 특수 텍스처/코어 | 폴리머 메쉬 또는 고밀도 폼 | 플래그십 성능 | $160–$250+ |

용어 “복합재 피클볼 패들” 이 용어도 발전했습니다. 엄밀히 말하면, 복합재는 여러 재료로 구성된 모든 구조를 나타내며, 기술적으로는 오늘날 시장에 나와 있는 대부분의 패들을 포함합니다. 그러나 일반 소매 용어로는 주로 폴리머 코어가 있는 유리섬유 면 패들을 설명하는 데 사용되며, 일반적으로 $50–$100 범위에 있습니다. 복합재 피클볼 패들은 초급 나무 모델에서의 접근 가능한 단계로 위치해 있습니다.

성능 비교 표

| 속성 | 그래파이트 | 복합재 (유리섬유) | 탄소 섬유 T700 |

|---|---|---|---|

| 무게 | 220–250g | 225–255g | 210–240g |

| 전력 전달 | 보통 | 중간-높음 | 높음 |

| 스핀 가능성 | 낮음-중간 | 보통 | 높음 (~유리섬유보다 30% 더) |

| 터치 / 느낌 | 단단하고, 적당한 피드백 | 부드럽고, 너그러운 | 깨끗하고 반응이 빠름 |

| 내구성 | 좋음 | 좋음 | 우수함 |

| 가격 계층 | 입문-중급 | 입문-중급 | 중급-프리미엄 |

| 이상적인 플레이어 프로필 | 초보자, 레크리에이션 | 초보자, 중급 | 중급에서 고급 |

시장이 응답했습니다: 탄소 섬유의 점유율

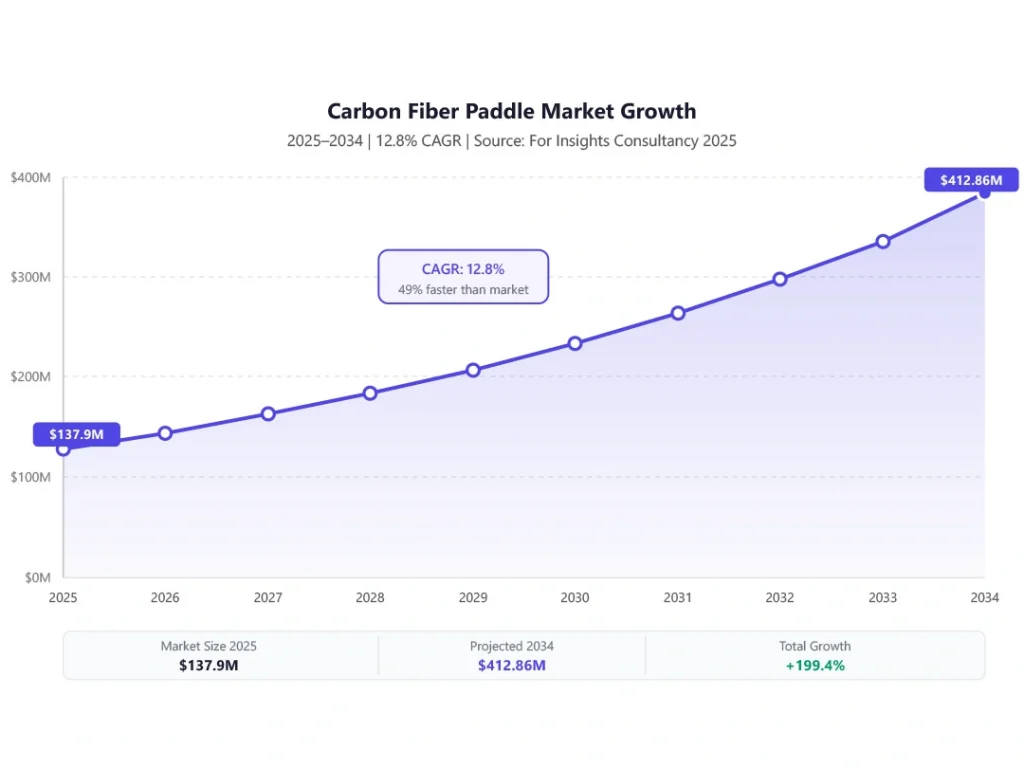

데이터는 모호하지 않습니다. 탄소 섬유 패들 세그먼트는 2025년 1억 3천 790만 달러, 연평균 14.8% 성장률로 성장 중입니다. 12.8% CAGR 로 평가되었으며, 예상 종료점은 2034년까지 4억 1천 286만 달러, For Insights Consultancy의 2025 시장 보고서에 따르면. 더 넓은 피클볼 패들 시장은 2026년부터 2032년까지 8.6%의 연평균 성장률(CAGR)로 성장하고 있습니다. (QY Research). 탄소 섬유는 전체 시장보다 49% 더 빠르게 성장하고 있습니다.

그 간극은 좁혀지지 않고 — 오히려 넓어지고 있습니다.

T700 가격 압축 효과

탄소 섬유가 중간 시장 재료가 된 이야기는 기술의 변화가 어떻게 이루어지는지를 보여주는 전형적인 사례입니다. 2021–2022년에는 T700 등급의 탄소 섬유 패들이 $180–$250의 프리미엄 가격이었습니다. 원자재 비용은 실제로 있었고, 제조 복잡성도 실제로 존재했으며, 소비자 인식은 아직 부족했습니다.

2025–2026년까지 모든 면에서 그 계산이 바뀌었습니다:

- 제조 규모: 중국 패들 제조업체들의 대량 생산이 T700의 생산 비용을 상당히 낮췄습니다.

- 소비자 이해도: 3년간의 피클볼 바이럴 성장으로 인해 T700의 의미를 아는 구매자가 생겼고, 이에 대한 기대가 생겼습니다.

- 브랜드 차원의 약속: 주요 브랜드들이 탄소에 대한 입지를 확고히 하여 카테고리의 정상화를 가속화했습니다.

신호 사건은 Selkirk의 2026년 2월 SLK Geo 출시였습니다 — T700 탄소 섬유 패들이 $100 소매가로판매되면서, 피클볼 장비에서 가장 신뢰받는 이름 중 하나인 Selkirk가 T700을 세 자리 숫자로 낮추면서 전체 카테고리의 소비자 기대가 재설정되었습니다.

새로운 경향을 정의하는 브랜드 움직임

브랜드의 움직임은 미세하지 않습니다. 그것들은 전략적 약속입니다:

- JOOLA: 모든 성능 라인에 걸쳐 롤링 CFS(탄소 마찰 표면) 기술이 적용되었습니다 — 스핀을 극대화하기 위해 설계된 거친 질감의 탄소 표면이 카테고리 차별 요인이 되었습니다.

- CRBN: 100% T700 도레이 탄소 섬유로 전체 브랜드 정체성을 구축했습니다; 다른 것은 제공하지 않습니다.

- Selkirk: 새로운 SLK 라인업(Geo, Dauntless, Valkyrie)은 $200 이하 가격대의 전 제품이 모두 탄소 섬유로 구성되어 있으며, 성능 제공에서 그래파이트가 사실상 제외되었습니다.

- Franklin: FS Tour는 성능 세그먼트의 겉면 재료로 탄소 섬유를 선택합니다.

그 브랜드의 움직임에서 누락된 점을 주목하세요: 그래파이트. 이러한 브랜드는 그래파이트 혁신에 투자하지 않고 있습니다. 대신 탄소 등급, 표면 질감, 코어 기술 및 열 성형 프로세스에 투자하고 있습니다.

결과적으로, 그래파이트는 $50–$120 진입 및 레크리에이션 범위에 자리 잡았습니다. — 합법적인 상업적 볼륨이 있는 층이지만 성능 층은 아닙니다. 이 세분화는 이해하는 것이 중요합니다 — 우연이 아닙니다. 이는 재료의 성능 한계가 어디에 있는지를 반영합니다.

2026년 B2B 구매자에게 의미하는 바

브랜드 소유자, Amazon FBA 판매자 및 도매업체가 2026년 제품 라인을 구축하거나 업데이트할 때 중요한 프레임은 다음과 같습니다:

그래파이트는 죽지 않았습니다. 재포지셔닝되었습니다.

이를 올바르게 사용하면 전략적 자산이 됩니다. 여전히 프리미엄 옵션으로 취급하면 부채가 됩니다.

2026년 그래파이트에 대한 상업적 제안

그래파이트 패들은 실제로 가치 있는 특정 상업적 기능을 수행합니다:

- 상단 고객 확보 SKU: $55–$85의 그래파이트 또는 복합 패들은 차이를 모르는 새로운 플레이어에게 적합한 진입점입니다. 저렴한 가격으로 고객을 확보할 수 있습니다.

- 레크리에이션 및 기관 볼륨: 공원 및 레크리에이션 프로그램, 리조트 대여, 초급 클리닉, 기업 팀 빌딩 이벤트 — 이러한 채널은 대량 구매를 하며 T700 성능이 필요하지 않습니다. 복합 피클볼 패들이 이 세그먼트를 지배합니다.

- 업그레이드 경로: 귀사의 브랜드에서 그래파이트 패들을 구입하고 긍정적인 경험을 한 플레이어는 12–18개월 이내에 귀사의 T700 또는 열 성형 SKU로 업그레이드할 가능성이 훨씬 높습니다. 이 평생 가치 계산은 브랜드 구축자에게 중요합니다.

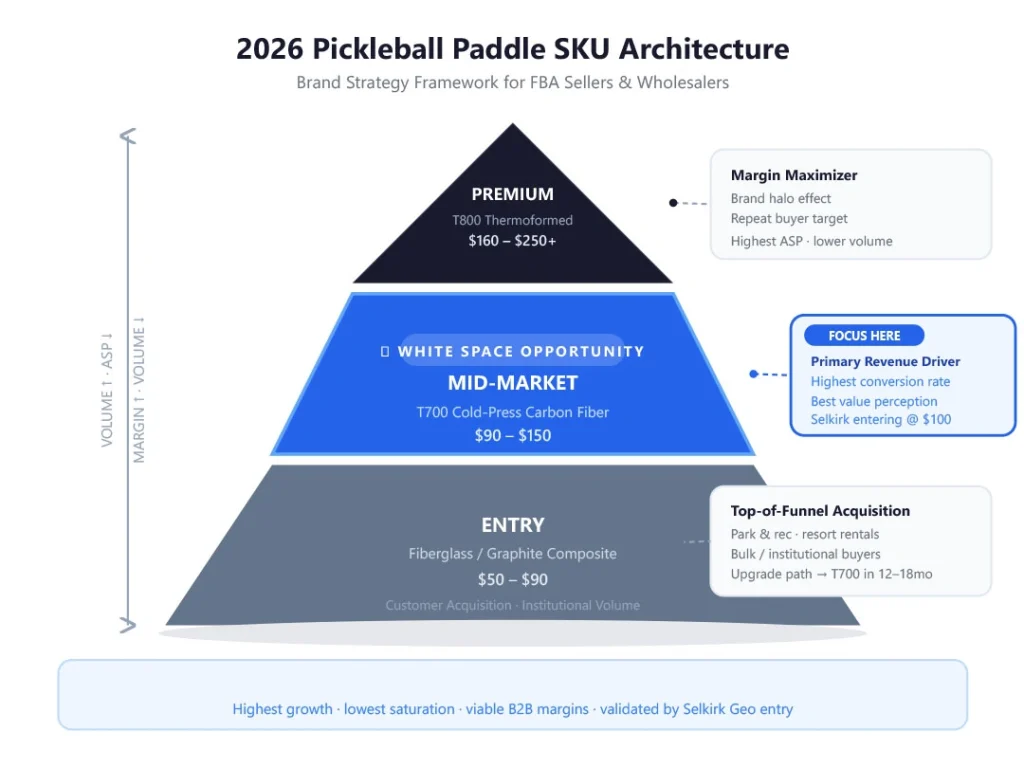

2026년 SKU 아키텍처 추천

2026년에 승리하는 브랜드는 세 가지 티어 제품 사다리를 운영하고 있습니다. 다음은 프레임워크입니다:

| 계층 | 5 × 5 × 2.5 cm | 가격대 (소매) | 전략적 역할 |

|---|---|---|---|

| 입문 | 유리섬유 또는 그래파이트 복합체 | $50–$90 | 고객 확보, 대량/기관, 상단 고객 확보 |

| 중간 | T700 냉압 탄소 섬유 | $90–$150 | 주 수익 원천, 최고의 전환율, 최고의 가치 인식 |

| 프리미엄 | T800 열 성형 탄소 섬유 | $160–$250+ | 마진 극대화, 브랜드 할로, 반복 구매자 목표 |

화이트 스페이스: 중간 시장 T700

특히 강조할 가치가 있는 세그먼트가 있다면 그것이 바로 $80–$130 T700 탄소 섬유 브래킷. 현재 시장에서 가장 높은 성장률과 가장 낮은 포화 지역입니다:

- Selkirk가 진입하고 있습니다 ($100 Geo), 이는 수요를 검증합니다

- 가장 확립된 브랜드는 여전히 $150 이상에 집중되어 있습니다

- T700을 $130 이하로 구매하려는 소비자의 의향이 높고 증가하고 있습니다

- 대량의 마진 프로필은 B2B에 유효합니다

아직 T700 콜드프레스 제품을 소싱하지 않는 FBA 판매자 및 브랜드 소유자를 위해, 이것이 2026년 여러분의 주의가 있어야 할 곳입니다. 그래파이트가 아닙니다. 열형성 플래그십이 아닙니다. 중간 시장 T700입니다.

NexaPaddle의 자재 사다리: 복합재에서 T700 성능으로

NexaPaddle의 제품 카탈로그는 위에서 설명한 계층 구조에 직접적으로 연결됩니다. 여기에서 라인업이 진입부터 플래그십까지 어떻게 진행되는지 확인할 수 있습니다:

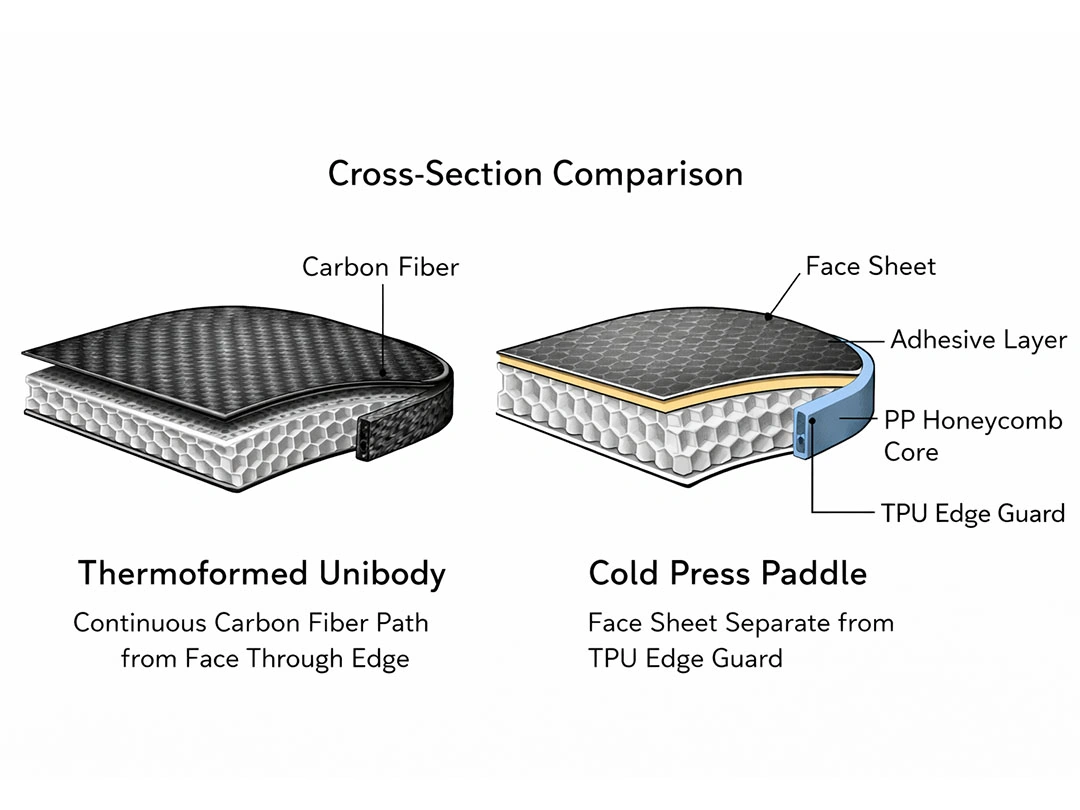

계층 1 — 진입: 콜드 프레스 유리섬유 (제품 1.1)

대량의 복합재 피클볼 패들에 대한 기본 SKU:

- 페이스: 유리섬유 | 코어: PP 허니콤 | 엣지: TPU

- 두께: 10mm / 13mm / 16mm | 무게: 220–245g

- 기능: 400×195mm (컨트롤) 또는 417×188mm (파워)

- 소매 범위: $25–$60 | 최소 주문 수량: 300 pcs

이것은 브랜드 번들, 스타터 세트 및 입문 수준의 소매 목록에 적합한 기관 대량 SKU입니다. T700 패들과 경쟁하는 것이 아닙니다; 다른 구매자를 확보하고 있습니다. TPU 엣지 가드는 높은 빈도로 사용되는 환경에서 필요한 내구성을 추가합니다.

계층 2 — 중간: 콜드 프레스 탄소 섬유 (제품 1.2)

성장하는 중간 시장을 목표로 하는 브랜드 빌더를 위한 상업적 스위트 스팟입니다:

- 페이스: 탄소 섬유 (UD 또는 3K 직조) | 코어: PP 허니콤

- 두께: 13mm / 16mm | 무게: 210–235g

- 기능: 400×195mm 또는 417×188mm (1.1과 동일한 툴링)

- 소매 범위: $60–$130 | 최소 주문 수량: 300 pcs

이것은 플래그십 생산 최소수량 없이 T700/탄소 섬유 카테고리에 진입하는 브랜드를 위한 제품입니다. UD (유니디렉셔널) 옵션은 파워와 공속을 강조합니다; 3K 직조는 소비자가 인식하는 더 전통적인 탄소 미적을 제공합니다. 표준 콜드프레스 구조에서 $60–$130의 소매 가격으로, 이것이 중간 시장의 대량이 존재하는 곳입니다.

→ NexaPaddle의 탄소 섬유 피클볼 패들 전체 콜드프레스 사양 및 맞춤형 옵션을 보려면.

계층 2+ — 프리미엄 중간: 열형성 T700 (제품 2.3 / 2.6)

열형성 계층은 건축 방법론이 제품을 의미 있게 구분할 수 있는 곳입니다:

열형성 T700 파워 (제품 2.3 / 몰드 #3)

- 페이스: 탄소 섬유 UD/3K 또는 T700 | 코어: PP 허니콤

- 구조: 엣지리스, 열형성

- 기능: 417×188mm | 두께: 13mm / 16mm | 무게: ~220g

- 소매 범위: $100–$180 | 최소 주문 수량: 100 pcs

핫 프레스 포지드 T700 (제품 2.6 / 몰드 #7)

- 페이스: T700 탄소 섬유 (UD/3K) | 열 프레스 성형 과정

- 기능: 420×185mm | 핸들: 145mm 연장

- 무게: 220–235g

- 소매 범위: $120–$180 | 최소 주문 수량: 100 pcs

열형성(핫프레스)으로의 전환은 페이스와 코어 간의 더 밀집되고 균일한 결합을 생성합니다 — 고성능 테니스 라켓과 여가용 라켓을 구분하는 동일한 원리입니다. 몰드 #3의 엣지리스 구조는 연구한 소비자에게 보이는 제품 차별화 요소입니다. MOQ가 낮다는 점에 유의하세요 (콜드프레스의 경우 300 pcs에 비해 100 pcs) — 이는 신규 SKU를 테스트하는 브랜드 빌더에게 중요한 장점입니다.

→ NexaPaddle의 전체 사양 및 맞춤형 옵션 열 성형 피클볼 패들 페이지를 방문하세요.

3단계 — 플래그십: GEN5 Gatling T800 (제품 3.5)

NexaPaddle 라인업의 헤일로 제품 — T800 탄소 및 차세대 코어 기술을 기반으로 구축:

- 페이스: T800 탄소 섬유 + 테플론 직조 표면 질감

- 코어: GEN5 고분자 에너지 반환 메쉬(독점)

- 그립: 폼 그립 + 3D 가죽 오버랩

- 기능: 419.5×188mm | 두께: 16mm

T800 탄소 섬유는 T700보다 인장 모듈러스가 높아 — 체중 단위당 더 많은 강성을 제공하여 접촉 시 더 정밀한 에너지 반환으로 이어집니다. 테플론 직조 표면 질감은 톱스핀 샷에서 공의 그립을 극대화하도록 설계되었으며, 표면을 거칠게 만들어 USAPA의 표면 거칠기 지침을 위반하지 않도록 합니다. GEN5 고분자 메쉬 코어는 표준 PP 허니컴보다 의미 있는 단계로 — 에너지를 흡수하는 것이 아니라 반환합니다.

이 SKU는 JOOLA, Selkirk Prime 및 Franklin의 플래그십 라인에 대항하여 위치합니다. 이는 브랜드 헤일로 제품이며 귀사의 제품 개발 능력을 입증하는 포인트로, 판매량을 증가시키는 요소는 아닙니다.

자주 묻는 질문

Are graphite pickleball paddles good for beginners?

Yes — with the right expectations set. A graphite pickleball paddle in the $50–$90 range offers a firm face with reasonable control, which is appropriate for players learning court positioning and shot mechanics. They’re better than wood or aluminum, and the price point keeps initial investment low. What they don’t offer is the spin potential and power transfer of T700 carbon fiber — but most beginners aren’t ready to use that performance anyway. As a first paddle or an entry-level SKU for a brand, graphite serves a real purpose.

What is the difference between graphite and composite pickleball paddles?

The terms are related but distinct. Composite pickleball paddles typically refer to fiberglass-face paddles with a polymer honeycomb core — the construction is straightforward and optimized for affordability and durability. Graphite paddles add a thin crystalline carbon coating or layer to a largely fiberglass construction, contributing added stiffness and a harder surface feel. In practice, both fall in the entry-to-mid price tier ($40–$130), and both are a step down from true woven carbon fiber in terms of spin potential and performance ceiling. Retailers sometimes use these terms interchangeably, which adds to the confusion, but from a sourcing and specification standpoint they represent distinct constructions.

Is carbon fiber better than graphite for pickleball?

For performance play, yes — unambiguously. Woven carbon fiber (particularly T700-grade) delivers meaningfully higher spin generation (~30% more than fiberglass/graphite), better power transfer, and a more consistent face stiffness due to the structural integrity of the woven filament sheets. At competitive play levels from 3.5+ on up, the performance gap is real and measurable. The price gap has narrowed substantially in 2025–2026 — T700 paddles now start around $80–$100 at retail — which removes the historical justification for choosing graphite over carbon fiber for performance-oriented buyers. For recreational play and bulk institutional use, graphite and composite paddles still make economic sense.

What is T700 carbon fiber and why does it matter?

T700 is a specific grade designation from Toray Industries — the Japanese materials manufacturer that dominates the high-performance carbon fiber supply chain. The “T” series denotes tensile strength: T700 delivers approximately 4,900 MPa 인장 강도, making it substantially stronger and stiffer than standard carbon fiber variants used in entry-level applications. In paddle terms, T700 means a face that can be thinner while maintaining stiffness, which allows manufacturers to optimize weight distribution and power transfer simultaneously. T700 became the de facto standard for performance pickleball paddles from 2022 onward. When a brand like CRBN says “100% Toray T700,” that’s a specific, verifiable material claim — not marketing language.

Can I still sell graphite paddles profitably in 2026?

Absolutely — if you position them correctly. The entry-level recreational segment is not small: beginner players, institutional buyers (gyms, parks, resorts), and bulk gifting channels all represent real volume for composite and graphite paddles. The key is not trying to compete on performance against T700 carbon fiber products, and not pricing graphite SKUs above ~$90 where consumer expectations shift. The most effective strategy is using a graphite or composite SKU as a customer acquisition vehicle — a $60–$75 branded paddle that performs appropriately for its price point and creates a buyer relationship you can upgrade. Where brands get into trouble is when graphite is their only SKU, or when it’s priced and marketed as a performance product. Within the right tier, graphite remains viable and commercially healthy.

결론: 그래파이트는 그 시대에 유용했으나 — 이제 전략적으로 사용하세요.

그래파이트는 피클볼 시장을 위해 해야 할 일을 정확히 수행했습니다: 폭발적인 성장 단계 동안 스포츠에 '프리미엄' 접근 가능한 진입점을 제공했습니다. 수백만의 선수들에게 그들이 정당화할 수 있는 가격으로 성능 패들을 소개했습니다. 이는 스포츠 발전에 대한 정당한 기여입니다.

2026년에는 그래파이트의 상업적 역할이 명확해졌습니다. 더 이상 프리미엄 티어가 아닙니다 — 탄소 섬유가 프리미엄 티어로, 5년 전에는 불가능해 보였던 가격에 판매되고 있습니다. 2025년 탄소 섬유 패들 부문이 1억 3천 7백 90만 달러에 달하며 매년 12.8% 성장하는 것은 일시적 현상이 아닙니다. 이는 소재 비용 압축, 제조 혁신 및 업계의 주요 플레이어들로부터의 브랜드 수준 약속에 의해 이끌어진 구조적 시장 변화입니다.

제품 라인을 구축하는 B2B 구매자에게 전략적 질문은 그래파이트 또는 탄소 섬유가 아닙니다. 그것은 두 가지를 일관된 제품 아키텍처에서 어떻게 사용할지를 고민하는 것입니다.:

- 고객 확보 및 기관 판매를 위한 입문 티어에서 그래파이트 및 복합체 사용

- 가장 높은 성장 수요 세그먼트를 포착하기 위한 중간 티어에서 T700 냉압착

- 마진 및 브랜드 포지셔닝을 극대화하기 위한 프리미엄 티어에서 T700/T800 열형성

그것이 2026년 플레이북입니다. 이를 실행하는 브랜드는 지속 가능한 위치를 구축하고 있습니다. 소재 진화를 무시하는 브랜드는 해결책 없이 평균 판매 가격이 압박받고 있습니다.

2026년 전체 소재 스펙트럼에서 귀하의 제품 라인을 구축할 준비가 되셨나요? NexaPaddle은 모든 티어에서 제조합니다 — 300개 MOQ의 냉압착 유리 섬유 및 복합 피클볼 패들부터 100개 MOQ의 열형성 T700/T800 플래그십 패들까지. 완전한 OEM/ODM 맞춤화 가능합니다.

NexaPaddle에 문의하기 2026년 소싱 전략에 대해 논의하려면.

USA Pickleball 2025 장비 기준 매뉴얼, 개정 3.0. 승인된 패들에 대한 공식 중량 제한은 명시되어 있지 않습니다. 승인 기준은 치수, 표면 질감, 소재 제한 및 굴곡 테스트에 중점을 둡니다.

표면 질감 및 강도 특성을 기준으로 한 T700 탄소 섬유 스핀 성능 비교; NexaPaddle 제품 개발 사양에서 참조되며 독립 패들 리뷰 출판물에서도 널리 보도되었습니다.

통찰력 컨설팅을 위해, 탄소 피클볼 패들 시장 규모, 동향 분석 연구 보고서, 2025년 10월. 시장 가치: 1억 3천 7백 90만 달러(2025), 예상 4억 1천 286만 달러(2034), CAGR 12.8%.

QY Research, 글로벌 피클볼 패들 시장 보고서, 2026년판. 전체 시장 CAGR: 8.6%(2026–2032).

Selkirk Sport 보도 자료, 'Selkirk, 완전히 새로운 SLK 라인업 발표', 2026년 2월 17일; The Dink Pickleball을 통한 확인된 보도, 2026년 2월 24일.